Abenomics: Modern Problems Require Modern Solutions

Abenomics: Modern Problems Require Modern Solutions

Revisiting Shinzo Abe’s Radical Policy to Revive the Economy

Introducing Inquisitorial by Indianaut, a long-form newsletter where we explain and analyze important stories stemming out of the Indian entrepreneurial ecosystem & economy. New articles every Saturday & Sunday.

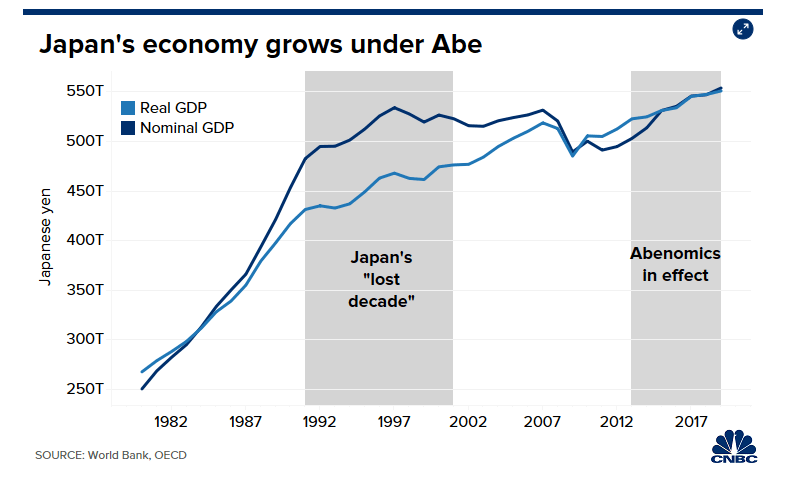

Japanese Prime Minister Shinzo Abe resigned last month from his position citing poor health. He has been succeeded by Yoshihide Suga who formerly served as Chief Cabinet Secretary. His resignation marks the end of an era for Japan. In 2012 when Shinzo Abe stepped in as the Prime Minister of Japan, the economy was in a dire situation and its GDP growth rate had tumbled to -4.3% and the euro sovereign debt crisis was in full swing. In 2012 the Organisation for Economic Co-operation and Development (OECD) Yearbook editorial stated that Japan's "debt rose above 200% of GDP partly as a consequence of the tragic earthquake and the related reconstruction efforts."

Shinzo Abe had the work cut out for himself. He devised a plan to use a detailed, growth-oriented strategy and change the very nature of how the Japanese economy functioned. This strategy popularly came to be referred to as “Abenomics”. Abenomics has “three arrows”: (i) aggressive monetary policy, (ii) fiscal consolidation, and (iii) growth strategy.

Abe believed that he could use this story for igniting Japan’s economy again by using the multiple levers that drive the Japanese economy by using them in tandem i.e. Structural Reforms, Monetary Policy & Fiscal Policy and, all working together, to achieve a single objective - Growth.

The Consumption Issue

Japanese economy faced some unique problems. Japanese consumers are meager spenders; they save a larger portion of their income that too in cash deposits. This made Japan an unattractive investment destination for private corporations. It also limits the number of buyers of private corporations’ equity and securities. The lack of demand for consumer goods also has an impact on the unemployment front. Thus, a policy was needed to alter Japan’s private saving Spree.

In 2013, the Japanese government injected about 10.3 trillion Yen in the market in order to improve infrastructure and generate more employment opportunities. In 2014, another 5.5 trillion Yen were pumped into this scheme focussed on building critical infrastructure projects, such as bridges, tunnels, and earthquake-resistant roads, hoping it would increase the demand for steel, vehicles, heavy machinery, etc. in the economy.

However, the problems didn’t end there, now the restricted flow of credit aggravated Japan’s problem. The reckless lending in the 1990s made Japanese banks reluctant to lend. This created problems for private corporations as access to credit or borrowed money is what drives most economies and encourages investment and expansion.

Consequently, the ruling government made an association with Japan’s Central Bank to increase the free flow of credit and make money more accessible to the people. As a result, the Bank of Japan (BOJ) cut the interest rates to zero & for a period even offered negative interest rates. A quantitative easing program was also initiated where the Central Bank. It included the adoption of a higher inflation target, more aggressive monetary easing including through the purchase of risk assets and longer-duration government securities, as well as improved communication and forward guidance. Bank of Japan closely monitored the stimulus to ensure that inflation does not rise beyond its targeted rate of 2%.

The Labour Conundrum

Another problem that Abenomics had to resolve was the shortage of labor in Japan.

Japan’s birth rate has been plummeting for many decades and it was expected that by 2060 the country would lose its over one-third of its population from 2015 level. The government spent over 2 trillion Yen on childcare, educational reforms, scholarships to ease the burden of children on parents and encourage them to reproduce. The government also tried to skill women so that they could reduce the immediate problem of the labor shortage and encouraged people to continue working past the age of 65.

The Ballooning Debt

While Abenomics involved an increase in government spending to support growth, the strategy also aimed to achieve a budget surplus and bring down debt over the long term. Japan’s government debt — at more than 200% of GDP — was already the highest among OECD countries. Back in 2012, it was even being speculated that “Japan could be the next Greece.” But the differences between Japan and Greece can be seen in the demand for government debt; more than 90% of Japanese government debt is held by domestic investors, whereas about 70% of Greek government debt is held by overseas investors.

In order to address the growing debt/GDP ratio and create a balanced budget, Shinzo Abe increased the consumption tax from 5% to 8% in 2014 to 10% in 2019. It will be interesting to see if the 10% tax is enough or if there is going to be a further increase in taxes. Given the aging population and rising costs on medical bills and social security schemes, the target of achieving a primary balance (“PB”) surplus was pushed back five years to FY2025 from FY2020.

Did it Work?

So that leaves us with the final question, how did Abenomics fare?

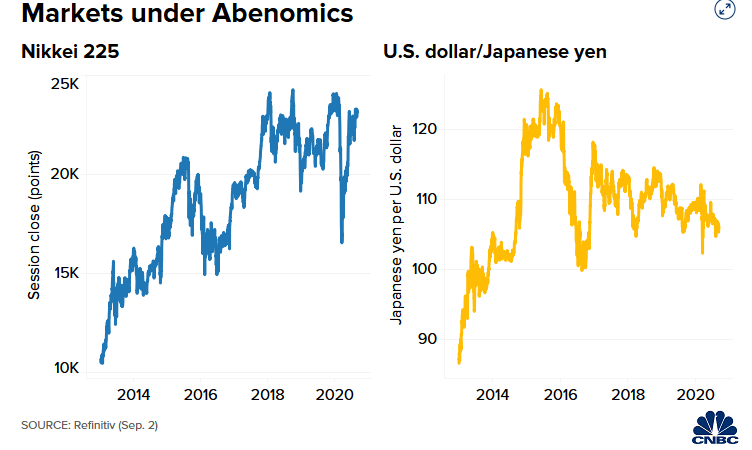

Well for starters, the unemployment rate in the country dropped to under 3% for the first time in 20 years. The economy was observed through a slow but steady growth rate until the pandemic crippled the equation altogether. On the other side, demand seems still to be drowsy. The policies failed to hit its target of 2% inflation and various economists believe that the spending spree which the government did also didn’t yield the desired results.

While an important goal of Abenomics was to stimulate consumption, the rising consumption tax proved to have a counterintuitive effect. While the legislation to increase tax had bipartisan support and tax was planned by a previous government, both Abe and the governor of the Bank of Japan (BoJ) Haruhiko Kuroda is to blame for the decision to implement it, leading to failure to achieve the desired goals.

All in all, just like most economic polices this too had some hits and some misses. But what Abe would remember for other than his policies is that he was never afraid of conceding to the people of Japan that the country had a colossal problem. He acknowledged the fact that there were gaps in the economy, and it needed some measures to rectify it and he was honest about it. Even if his economic policies did not have the intended effect, he dared to try out new things. And hopefully, that will be his lasting legacy.

Lessons for the World

Can other countries take a cue from the Abenomics?

As Adam S. Posen states, we can learn the lesson is that policy change is always possible, but ambition is required. There will always be reasons not to implement reforms, the biggest one would be lack of political will. With no fundamental change in the party system or the form of government, the action is shown to be indeed possible.

Abenomics shows that there is nothing wrong with central banks cooperating with fiscal authorities. There can be a relationship of constructive cooperation between the Central Bank and the government. Strong policy coordination among different branches of the state, communication, and guidance to the general public about government policies can play a crucial role in determining whether a policy will be a success or failure.

Japan shows that the returns on tackling the underutilization of human capital in Japan dwarf the impact of everything else, including the problem of a declining workforce. If Japan were to get more of its university-educated women into the workforce, the demographic problem would go away for decades. The participation of women in the labor force is not only needed for economic growth but also to create an equitable society.

There are lessons for India too. The post-pandemic world appears to be very different from what it was. On the monetary policy front, the MPC and inflation targetting approach of RBI creates stability, takes into account the government’s view, and allows people to forecast future policies to a reasonable degree. However, outside that, there are far too many examples of poorly thought-out ideas being hastily implemented without prior notice to the public like demonetization or country-wide lockdowns. Implementation of reforms not only needs political will, constitutional power, and majority votes in the Parliament but also the support of the general public, especially those who are affected by it. We should try to avoid these pitfalls in the future, exploit our demographic dividend to the fullest, and formulate a version of Abenomics that works for us.

Special Thanks to Paras Jatana for research.